Fintech companies are rapidly gaining momentum, but a persistent question remains: can financial inclusion and profitability coexist? Financial inclusion aims to open the doors of the banking system to those historically excluded, but let’s face it—what good is inclusivity if we can’t sustain the business model? For years, this question has lingered, but the answer is clear today: yes, it is possible.

To understand how Fintech companies have thrived in emerging markets and taken financial inclusion to the next level without sacrificing profitability, we explore key factors that are not only transforming the game but also redefining what it means to be profitable while providing access to all. This article is based on the first episode of our digital content series Conexión Fintech, co-produced by Finnosummit and Mastercard, where we dive deep into how Fintechs can strike this balance and turn financial inclusion into a sustainable business opportunity. You can watch the on-demand video here, or listen to the podcast on your favorite platform.

What Does It Mean to Be Inclusive?

Being inclusive is not just a social objective—it’s a responsibility. Fintechs have broken down physical and economic barriers that traditionally kept the unbanked out of the financial system. In Latin America, for example, mobile technology has played a pivotal role in opening these doors. Platforms like Mercado Pago in Argentina and Pix in Brazil have revolutionized the way consumers transact, making banking accessible through mobile phones, especially in regions with limited banking infrastructure. Mobile banking is here to stay, and its impact has been profound.

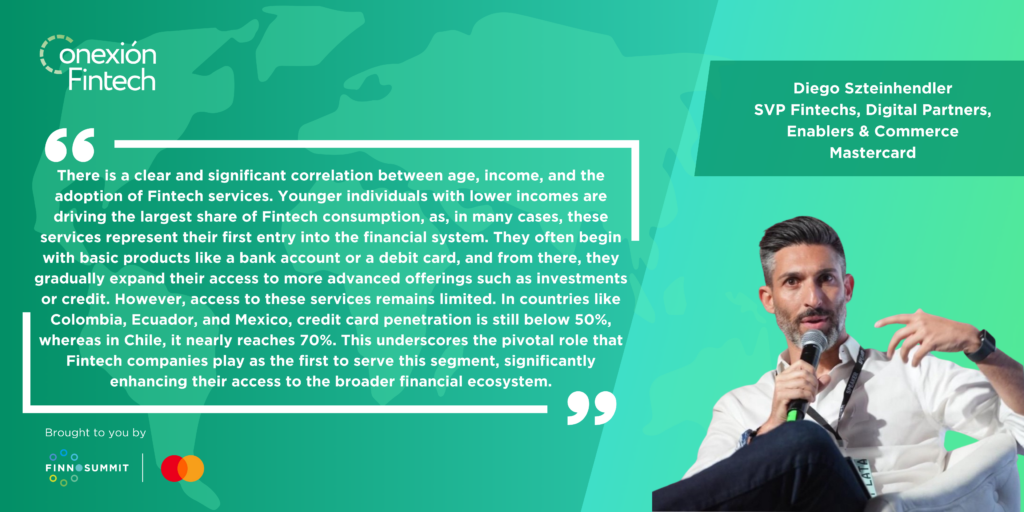

Additionally, Fintechs are reaching a critical segment: younger individuals and those with lower incomes.

Yape and DaviPlata have been pivotal in financial inclusion in Peru and Colombia, respectively. As of August 2024, Yape had over 12.3 million active monthly users in Peru, while DaviPlata reached 16.4 million clients by Q2 2023 in Colombia, improving access to financial products and services in both countries.

These platforms have successfully eliminated traditional barriers by offering intuitive and accessible interfaces. This has allowed millions of users to make transfers and payments without the need for a traditional bank account. Furthermore, strategies such as waiving digital transfer fees have promoted widespread adoption of electronic payments.

However, 60% of purchases in lower-income segments are still made in cash, posing a significant challenge to digitization. Fintechs are leading the charge by offering user-friendly experiences, making it easier to transition to digital payments. According to a Mastercard survey, between 40% and 60% of users accessed financial products for the first time through a Fintech, opening the door to innovative services like cryptocurrencies, investment opportunities, and credit.

Financial inclusion is not just a challenge—it’s a tremendous opportunity to build a more equitable, efficient, and digital ecosystem.

Profitability: The Holy Grail of Fintechs and the Power of AI to Scale Without Sacrificing Efficiency

Profitability remains the ultimate challenge for Fintechs, and the key lies in finding the right formula—lower costs, cutting-edge technology, and a scalable business model. But, this is not about sacrificing innovation. A perfect example is Nelo, which has successfully doubled its business size in just one year thanks to artificial intelligence. Yes, you read that right! AI not only optimizes processes but enables a company with just 35 employees to generate nearly one million dollars per person.

Fintechs that have strategically embraced technology have been able to reduce operational costs while scaling. By automating key processes such as credit evaluation and customer service, they not only improve profitability but also offer a much more efficient and personalized user experience. This is the secret to staying competitive in today’s fast-paced world.

Digital Financial Education: Empowering the Next Generation of Users

We cannot overlook one of the fundamental pillars of financial inclusion: digital financial education. In Latin America, Fintechs like Fintonic and Albo are driving change by providing tools that empower users to better manage their personal finances.

For example, Fintonic allows users to manage their income and expenses while learning the basics of savings and financial planning directly from the app. This not only helps users become more aware of their financial habits but also equips them with the knowledge to make more informed decisions.

Similarly, Albo in Mexico integrates financial management with practical guides and tips for better money management. Furthermore, initiatives like Destácame in Chile and Mexico are advancing financial inclusion by helping users understand and improve their credit scores, offering personalized education and actionable recommendations to improve their financial situation.

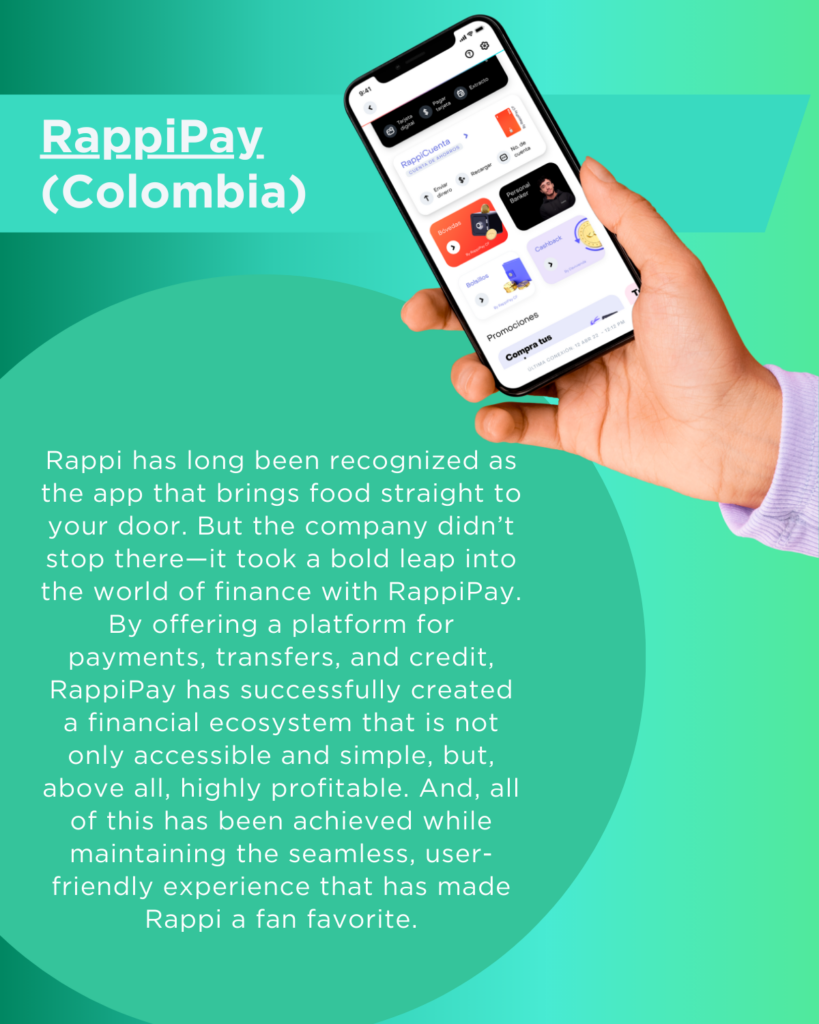

Success Stories: Who’s Leading the Charge in Latin America?

It’s not just theory—let’s look at real-world examples of Fintechs achieving what many once thought impossible: combining profitability and access for all.

What Does the Future Hold?

Financial inclusion and profitability are not opposing forces—they are two sides of the same coin. The Fintechs that balance both will be the ones that emerge victorious. As technology and innovation continue to evolve, we’ll see more companies breaking down the barriers of the traditional financial system and opening doors to prosperity.

The key, as always, is knowing when and how to innovate, while never losing sight of the ultimate goal: creating value for customers while building a sustainable business. And for those still skeptical, let me leave you with this thought: the future waits for no one, and Fintech is proof that when you have a clear mission, you can change the world.

We want to hear your success stories!

If you’re part of a Fintech that’s making a difference in financial inclusion, with a focus on profitability and the use of innovative financial technology, we invite you to share your story! Send your success case to info@finnosummit.com and tell us how your company has contributed to the democratization of financial services through accessible and sustainable technological solutions.